|

The Coinage Act of 1965 eliminated silver from the composition of U.S quarters and dimes and reduced the amount of silver in the half dollar to 40%. Until that point, half dollars, quarters, and dimes were all 90% silver. When the U.S Mint decreed that U.S. coins would be comprised of less valuable metals, they effectually lowered the real value of future coins printed by the Mint. Pre-1965 dimes and quarters quickly disappeared from circulation as citizens stockpiled the now historic coins for their metal value. This caused a coin shortage in years to follow, Gresham's law at work once again.

What happened to the composition of the U.S nickel? It remains the same, 75% copper / 25% nickel. Comprised of common industrial metals, the U.S nickel has a measurable underlying raw metal value that fluctuates with the market prices of nickel and copper. We believe current political and market trends make the U.S nickel an interesting investment consideration for all U.S. citizens. In February 2011, with high commodity prices, the raw metal in a nickel was worth 7.38 cents, 148% of its value. This meant the U.S. Mint was losing money on the production of each nickel, even before considering overhead costs. The U.S Mint quickly became aware of this situation and began considering solutions to ensure the underlying value of the U.S nickel remained below 5 cents. See this 2012 report released on their analysis of possible alternatives. With the current extended bear market in commodities, the raw metal in a nickel is now worth 2.77 cents. This has taken pressure off of the U.S Mint, however if the prices of copper and nickel were to rise, the rising underlying value of the U.S nickel will likely quicken the U.S. Mint's efforts to change the composition of the coin. We believe that similar to pre-1965 dimes and quarters, U.S. nickels would drain from circulation if the composition was altered to a less valuable alloy. An investor who holds stores of U.S. nickels may someday see the underlying value of these coins skyrocket as they gain intrinsic value years down the road, similar to pre-1965 dimes and quarters today. In addition U.S nickels provide indirect exposure to both the copper and nickel markets, as it is currently illegal to smelt legal U.S tender.

0 Comments

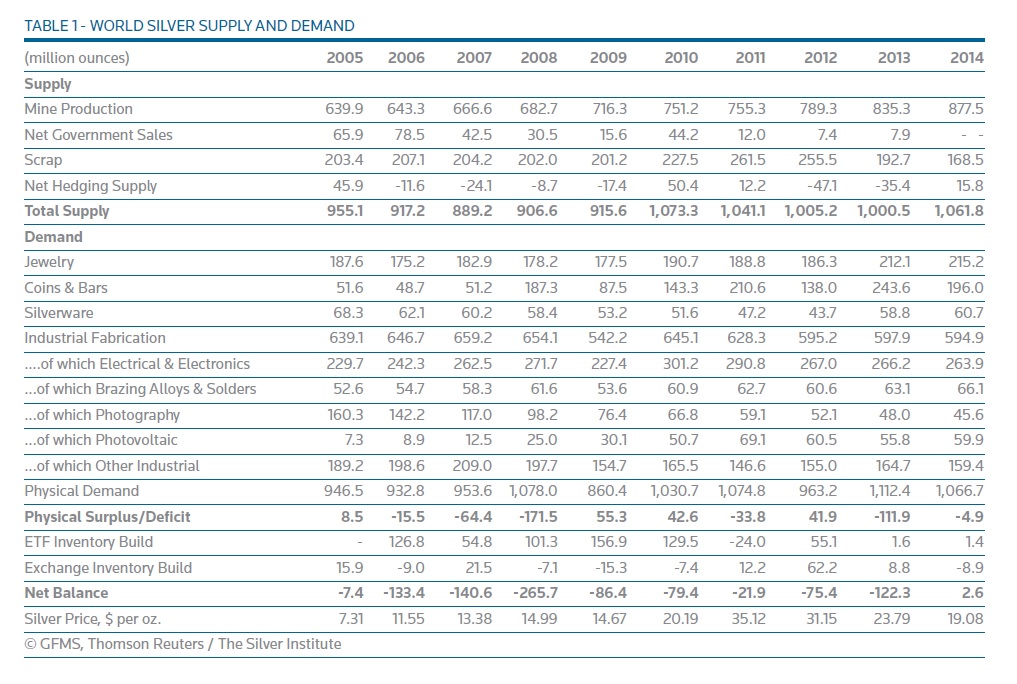

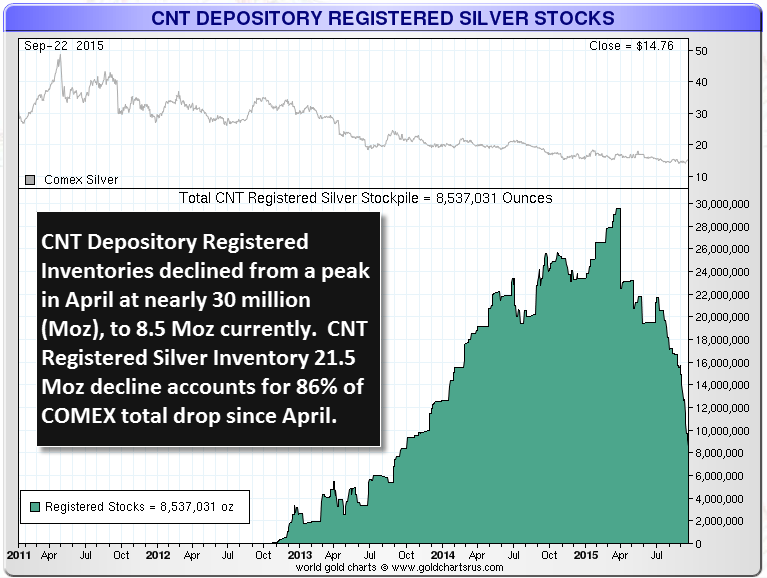

To follow up on our recent "Paper Markets in Metals" article, we at TFL Holdings decided to take a look at the forces shaping supply and demand in the silver market. We believe there to be a disconnect between the physical silver market and the market for silver future contracts on COMEX. As you will see below, growth of the global silver supply is constrained with evidence that demand for physical silver is increasing, yet prices remain relatively static. Silver is a rare geological deposit with many industrial applications. Unlike gold, the majority of silver produced each year is consumed by industry. Based on the supply and demand data provided below, there was a net physical deficit of 253.7 million ounces of silver during the years 2005-2014, not including inventory changes. In 2015, the price of silver continued to fall. Most estimates place the all-in cost of producing an ounce of silver well-above the current market value, forcing a further slide in production as mining operations shut down. This downward pressure on supply has been compounded by similar decreases in the prices of other metal ores mined concurrently with silver. See "Something Broke in the U.S. Silver Market" for a full analysis of the supply issues at hand.   Beyond changes to supply and demand in the physical market, recent developments in the silver futures market may also serve as a catalyst for price shocks going forward. As you can see from the chart below, registered silver is leaving the COMEX at an alarming rate. How is this trend playing out in recent weeks? COMEX registered silver plunged 10%, or roughly 3.5 million ounces, on January 4th, 2016, reflecting year end movements. This could be interpreted as Gresham's Law taking effect, as physical silver (good money) is chased out of the highly-leveraged futures market (bad money).  The point here, is that even though there is accelerating demand for physical silver with a probable supply crunch in coming years, the market price isn't rising. We believe this is due to large short positions held by institutional commodities traders in the futures market. The same institutional traders who are grossly short silver may have recently woken up to the underlying shift in market sentiment and are quietly taking delivery of as much physical silver as possible at these artificially low prices. Knowing the futures market will seize on the slightest increase in deliveries, they are then removing this silver from registered inventories and therefore, potential delivery on their short bets. If the market crashes up, and their shorts need to be covered, they can then shrug their shoulders and say they don't have the silver to deliver, settling their losses in cash. Sound like thievery? This is within the rules. Pay attention to all the new COMEX disclaimers popping up in 2015..  I would like to take a second today to discuss a developing trend in metals future markets that I find very disturbing. I will use Gold Futures (GLD) as an example, but this situation presents itself in silver, platinum and palladium markets to differing degrees of severity. A "future contract" is defined as a financial contract obligating the buyer to purchase an asset (or the seller to sell an asset), such as a physical commodity or a financial instrument, at a predetermined future date and price. In today's market, there is a growing disparity between the amount of gold being traded via these future contracts and the physical store of gold backing the transactions. Of the 415,220 gold futures contracts open on COMEX as of year end, 279,966 are set to expire in February (almost 70% of the total). This represents transactions for 27,996,600 troy ounces of gold settling in one month alone. Obviously this number is dynamic, meaning that as the February exercise date draws near, the vast majority of these contracts will be closed. This is due to traders utilizing gold futures as a hedge against various market risks with no intention of ever receiving physical gold. Due to the use of gold futures as derivatives by traders, a historic average of around 1% of all open contracts are physically delivered. To meet these deliveries, COMEX holds both "registered" and "eligible" physical gold stock. Eligible gold is any physical gold held at one of the COMEX-approved warehouses (HSCB Bank, Brinks Inc., Scotia Mocatta Depository). This gold is eligible for the settlement of gold future contracts, however it isn't set aside for that purpose. In other words, stores of 'eligible' gold may be intended for a purpose completely unrelated to settlement of future contracts open on the exchange. It is highly unlikely that 100% of eligible gold would be available for settlement in a crisis. Registered gold at COMEX is eligible gold that has been specifically delivered onto the exchange for settlement. See the below graph.  As you can see, levels of "registered" gold in COMEX vaults have been diving ever since Germany made its first gold repatriation request in 2013. As of 12/31/15 there are only 275,915 troy ounces of registered gold on hand at COMEX. Backed by 6,137,571 ounces of "eligible" gold at member banks, this totals roughly 6.5 million troy ounces of gold available for delivery in the best case scenario. However since eligible gold can still be utilized as collateral for other debt, it's highly unlikely it will be available for settlement in a crisis.

Under current conditions, gold futures are utilized by traders as a hedge against market risk. They do not anticipate delivery on these contracts and close them before the exercise date. There is currently 1 ounce of "registered" gold on hand for every 150 ounces traded via open future contracts. Even if only 1% of the currently open February contracts deliver, the delivery would be equal to the entire registered reserve at COMEX. I am not saying that delivery on gold futures will default in February, but the chance of deliveries on gold future contracts exceeding the amount of "registered" gold reserves in any one month is increasing. If conditions ever warrant a change of sentiment with regards to the delivery of physical metal, this market is sure to see a "run on the bank" scenario as parties default on delivery under their contracts. If you are an individual investor interested in owning gold, make sure to acquire physical coin and bullion, not a piece of paper. While recently purchasing a new domain name on GoDaddy.com, I noticed something interesting about their pricing model which gives great insight into how they value the registration of web domains. In most service industries, customers receive a discounted rate when signing up for a longer service period (think magazine subscriptions), meaning you'd pay less per year for a 5-year subscription than you'd pay for a 1-year subscription. In retail or manufacturing, this would be synonymous to a quantity discount. Such is not the case in the domain registration space. Wholesale domain registrars such as GoDaddy.com follow an inverted pricing model in which the annual fee for a 5 year domain registration is more than double the 1 year fee. The following pricing data was taken directly from GoDaddy to illustrate this point. Annual web domain registration fee 1 year - $12.99 per year 2 years - $21.49 per year (65% increase) 3 years - $24.32 per year (87% increase) 5 years - $26.59 per year (105% increase) Why does GoDaddy allow customers to register their website for one year at a price of $12.99, yet charge double the annual rate to lock down the site for 5 years? Why doesn't everyone just register on an annual basis to get the cheapest price? The value in establishing a long term web presence can only be part of the answer. With the domain registration market constrained by the supply of marketable domain names, there is no guarantee that these valuable assets will stay cheap forever. What if the price to register the same website is $49.99 next year? Or even $99.99? For the same reason homeowners are willing to buy the land their house is built on, growing businesses are willing to pay more in order to secure their online property and hedge against changes in the price of internet real estate. For CPAs renewing their licenses in California, the CPE requirements have become increasingly complicated over the last years. I wrote this article to help Californian CPAs better understand their annual continued education responsibilities and maintain their active license status.

Starting with the most general requirement, all California CPAs are required to complete 80 CPE hours in the two years leading up to the applicant's renewal date, with at least 20 hours completed EACH YEAR. Meaning no cramming 80 CPE hours into the week before you apply for renewal... They're onto us. Now of the 20 CPE hours required each year, 12 of those hours must be in technical fields defined by in Section 88(a)(1) of the CBA requirements. "Technical" is defined as accounting, auditing, fraud, taxation, consulting, financial planning, ethics (as defined by Section 87 (b), computer & IT (no word processing folks), and specialized industry or government practice training. Basically as long as the training focuses on the maintenance and enhancement of your skills, knowledge, & competency. If you notice, by fulfilling your technical requirement, you also meet the 24/80 Accounting & Auditing or Governmental requirements. Nicccce. In addition to enacting minimum annual CPE requirements, the California Accountancy Act requires all active CPAs who perform the majority of field work on financial/compliance audits of governmental agencies (Governmental Requirement), or provide attestation services (Accounting & Auditing Requirement) to complete 24 of 80 CPE hours in fields related to financial reporting. Now if you're a sucker for efficiency like myself, you'll be able to knock out the 24/80 requirement utilizing your 12 annual "technical" hours. However, If you are subject to the 24/80 requirement, an additional 4 hours of fraud CPE is mandated each renewal period. Just to clarify, you are responsible for 4 fraud CPE hours IN ADDITION to the 24 financial reporting CPE hours completed. This will have to be done separate from your 12 annual "technical" hours. The California Board of Accountancy also requires 4 hours of ethics CPE every renewal period. Basically, just make sure you fit some ethics courses into your 12 annual "technical" CPE hours. Also renewing CPAs are required to complete a board-approved two-hour "Regulatory Review" course every six years (based on the old ethics reporting cycle). This course covers the California Accountancy Act, California Board of Accountancy regulations, and enforcement of the Act. If you're like me, this babushka doll of requirements makes your head spin... here's a checklist laying it all out. 80 CPE hours each renewal period -24 related to financial reporting*

With the Dow Jones Industrial Average (DJIA) and S&P 500 (GSPC) consistently topping record highs during the last year, its hard not to wonder how long the stock market can remain in an uptrend. As an individual hesitant to put my minimal spare funds into equities, I found a cost-efficient way to produce valuable assets online. After first becoming interested in owning a piece of the internet, I learned that for a small fee ($2.99-$12.99), I could register a domain name through an accredited registrar for a specified number of years. In addition, I would have the option to renew the registration before it went to open auction at the end of the term. I immediately recognized the potential of such a low-cost investment. Instead of buying one share of Google stock (GOOG), I could register over 100 domain names, each with the potential to display content, share information, and provide services. Contrary to popular belief, the internet is not one large, synonymous platform. Beyond the explosive growth of the web during the dot-com boom, the Internet Company for Assigned Names and Numbers (ICANN) has continued to enhance competition, innovation, and consumer choice in the Domain Name System. The growth of country-code and generic top-level domains has fueled the domain registration market and increased the complexity of the internet. Since 1985, ICANN has assigned two-letter, ccTLDs to countries, sovereign states, and dependent territories, to be developed with limited restriction on their usage. Some countries have elected to restrict registration of domain names to citizens of the country. Others have taken a free market approach and appointed the administration of their TLDs to private industry. Under the administrator, .CO Internet S.A.S, domain registration on Columbia's .co ccTLD is now universally granted and has found popularity among small businesses. Through the registration of ccTLD names, it is possible to reach any geographic, cultural, or linguistic audience worldwide. The majority of internet users are familiar with the generic top-level domains (gTLDs) .com, .edu, .org, and .net. However, in June 2011, ICANN's Board of Directors authorized the launch of a new gTLD program meant to "encourage global participation in the technical management of the internet". 1930 total applications were accepted with a possibility for over 1300 new TLDs in the near future. Included in the plan was the implementation of internationalized domain name top-level domains (IDN ccTLDs). IDNs are a type of ccTLD which consist of language-native characters and utilize non-latin roots such as Arabic or Chinese. New IDN ccTLDs expand the linguistic base of the internet and are sure to generate future web activity in areas where English is not common. gTLDs give the internet a new flexibility, allowing for websites to organize by culture, language, interest or industry. As generic top-level domains expand the domain registration market, there is an opportunity to participate in the organization of new top-level domains and their connection to the current internet infrastructure. The diversity of the internet allows an investor to build a web portfolio with exposure to a combination of cultures, industries, and demographics. As the world's population continues to increase the demand for online services, entertainment, and information, I encourage investment in the supply of online content through the registration of domain names. |

AuthorTyler Logsdon is a CPA and Registered Securities Representative located in Newport Beach, California. He is actively employed in the blockchain industry. Categories

All

Archives

October 2018

ALL CONTENT IS PROVIDED FOR INFORMATIONAL PURPOSES ONLY. TFL HOLDINGS ASSUMES ALL INFORMATION TO BE TRUTHFUL AND RELIABLE; HOWEVER, THE CONTENT ON THIS SITE IS PROVIDED WITHOUT ANY WARRANTY, EXPRESS OR IMPLIED. NO MATERIAL HERE CONSTITUTES "INVESTMENT ADVICE" NOR IS IT A RECOMMENDATION TO BUY OR SELL ANY FINANCIAL INSTRUMENT, INCLUDING BUT NOT LIMITED TO STOCKS, COMMODITIES, OPTIONS, BONDS, FUTURES, OR BULLION. ACTIONS YOU UNDERTAKE AS A CONSEQUENCE OF ANY ANALYSIS, OPINION OR ADVERTISEMENT ON THIS SITE ARE YOUR SOLE RESPONSIBILITY.

|

RSS Feed

RSS Feed